The Myth of the “Perfect” Budget

Let’s be real for a moment. Have you ever spent a Sunday afternoon fired up with motivation, meticulously creating the “perfect” budget? You’ve got the spreadsheet, the categories, the fancy app—this time, you think, it’s going to stick. A week goes by, maybe two, and then… life happens. A surprise dinner out, an impulse buy, and suddenly that perfect spreadsheet is a monument to your guilt. Sound familiar?

If you’re nodding along, we have some good news. The problem isn’t you. It’s not your lack of willpower or discipline. The problem is that traditional budgeting is fundamentally broken because it’s designed by robots, for robots—not for actual, living, breathing humans. It ignores the messy, beautiful, and sometimes irrational world of human psychology.

This is where the behavioral budget comes in. It’s a complete rethink of how we manage our money, moving away from stressful restriction and towards effortless systems. In this guide, we’ll unpack why your old methods were doomed from the start and show you a simpler path to achieving true financial wellness. It’s time to ditch the guilt and start building a money system that actually works with your brain.

Why Your Old Budget Was Destined to Fail: 3 Psychological Traps

Before we can build a better system, we need to understand why the old one consistently lets us down. Our analysis shows that traditional budgeting methods stumble right into a few well-known psychological traps. Seriously though, it’s like they were designed to make us feel bad about our spending.

1. Decision Fatigue is Real, Folks

Think about your average day. You decide what to wear, what to eat for breakfast, which route to take to work, how to answer that tricky email from your boss. Every single choice, big or small, chips away at a limited resource: your willpower. Psychologists call this “decision fatigue.”

Now, add a traditional budget on top of that. Should you buy the name-brand coffee or the generic? Is this oat milk latte a “Groceries” expense or “Fun Money”? By asking you to track, categorize, and judge every single purchase, these budgets force you to make hundreds of extra micro-decisions. By the end of the day, your decision-making muscle is exhausted, which is precisely when you’re most likely to say “forget it” and order a pizza.

This phenomenon is closely related to a concept in psychology called “ego depletion.” Think of your self-control as a muscle. Every time you use it—whether to resist a donut or categorize a $3 purchase—you tire it out. A traditional budget forces you to do hundreds of these mental reps before you’ve even dealt with the day’s real challenges. It’s a workout you never signed up for, and it drains the very willpower you need to make smart financial choices when it truly matters.

2. The Pain of Restriction (And the Inevitable Rebound)

Traditional budgets are all about what you can’t do. Don’t spend more than $50 on dining out. Cut your coffee budget. Stop buying books. This approach frames money management as an act of deprivation. It feels like a crash diet—and we all know how those end.

When we feel overly restricted, our brains fight back. It often leads to a “rebound effect,” where after a period of intense control, we snap and go on a spending spree to compensate. This creates a toxic cycle: restrict, splurge, feel guilty, restrict even harder. This is a one-way ticket to constant financial anxiety, not financial freedom. The whole approach gets tangled up in the mental gymnastics of cognitive dissonance, where our desire to save clashes painfully with our actions.

This constant feeling of “not enough” pushes our brains into what psychologists call a “scarcity mindset.” When your mind believes resources are scarce, it can’t focus on long-term planning. Instead, it becomes obsessed with the immediate thing it can’t have, amplifying cravings and making impulsive decisions more likely. By telling you “no” all the time, traditional budgeting inadvertently makes you more focused on spending, not less. It’s a counterproductive cycle that keeps you trapped, making financial anxiety a core feature of your daily life, not a bug.

3. It’s Reactive, Not Proactive

Here’s the kicker with most budgeting apps: they are fantastic at telling you what you’ve already done wrong. You get a notification—“You’ve exceeded your restaurant budget!”—the morning after you’ve already enjoyed the meal. Well, thanks for the guilt trip, but it’s a little late now, isn’t it?

This is a reactive system. It reports on past actions, which only serves to create shame. It doesn’t proactively set you up for success. It’s like a smoke alarm that only goes off after the house has already burned down. A truly effective system needs to be proactive, shaping your behavior for the better before the spending happens.

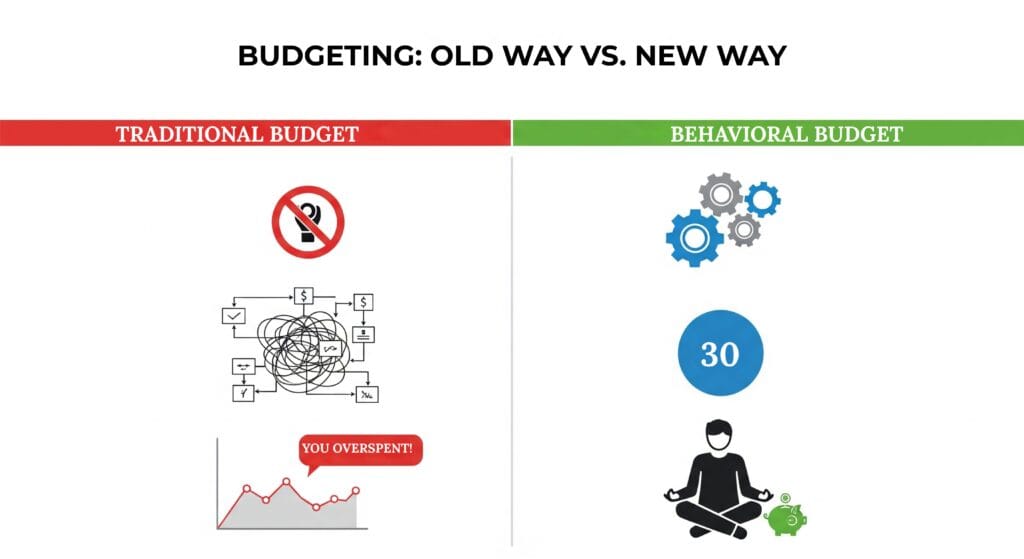

The Behavioral Budget: A 3-Step System for Financial Clarity

Okay, enough about the problem. Let’s build the solution. The behavioral budget isn’t about more rules; it’s about a smarter, simpler system. It’s designed to be proactive, reduce decision-making, and eliminate guilt. It only has three steps. That’s it.

Step 1: Automate Your Essentials (Pay Yourself First)

This is the cornerstone of the entire system. Instead of worrying about saving what’s left at the end of the month, you save first. The day your paycheck hits your account, you’ll have automatic transfers set up to move money where it needs to go. This is the ultimate “set it and forget it” automation strategy.

Here’s how it works: Calculate the total of your non-negotiables. This includes:

- Future You: Contributions to a high-yield savings account, retirement fund, or other investments.

- Essential Bills: Fixed costs like rent/mortgage, utilities, car payments, and insurance.

Set up recurring transfers to move this money out of your main checking account automatically. By doing this, you’ve met your most important financial goals without lifting a finger. This is the modern application of the timeless principle to Pay Yourself First. You’re building your financial future on autopilot.

We call this the “401(k) effect.” Most people successfully save for retirement because the money is taken out of their paycheck before they can even touch it. Out of sight, out of mind. The behavioral budget simply applies this incredibly powerful principle to your entire financial life. For a starting point, you can loosely adapt the 50/30/20 rule: aim to automate 20% to savings/investments and ~30% for fixed bills. The key is making your most important goals effortless by default.

Step 2: Define Your “Flexible Spending” Number

After your automation has whisked money away for savings and bills, look at what’s left in your checking account. That number? That’s it. That is your guilt-free, flexible spending money for the rest of the month (or until your next paycheck).

Not even kidding, this is a total game-changer. You no longer have 20 different categories to track. You don’t need to feel guilty about buying a coffee because it might eat into your “entertainment” budget. If you have the money in your account, you can spend it. This single number simplifies your financial life, drastically cutting down on decision fatigue. It gives you freedom within a framework.

“But what about big, planned expenses like a vacation or a new laptop?” This is where you can create specific, automated “sinking funds.” Simply set up another automatic transfer—say, $50 a month—into a separate savings account labeled “Vacation Fund.” This way, you’re saving for big goals proactively without impacting your daily flexible spending number. It turns a future source of stress into a simple, automated background process, which is a core tenet of mindful automation.

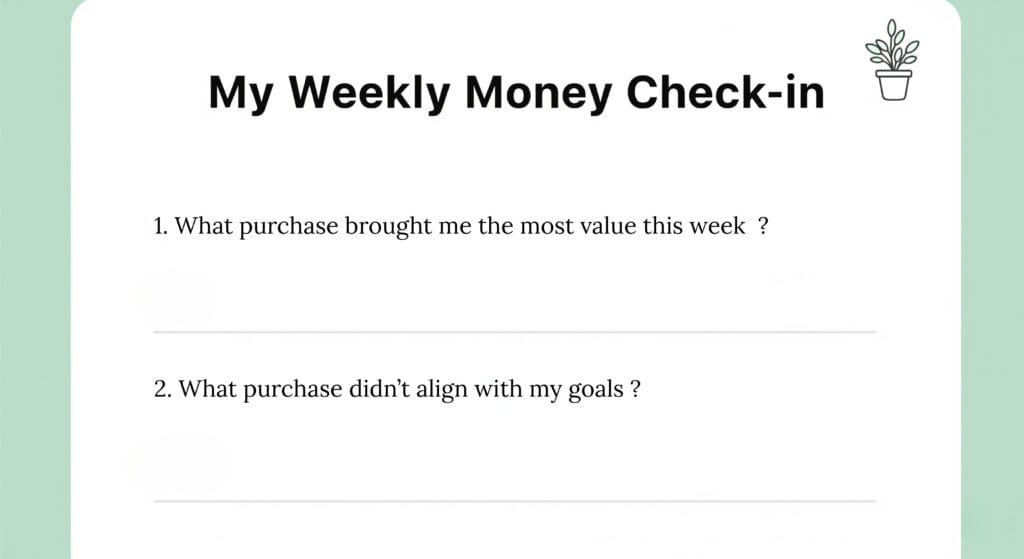

Step 3: Practice Mindful Spending Check-ins

This is where the “behavioral” part of the behavioral budget really shines. Instead of tedious tracking, we’re going to build awareness through reflection. Once a week—maybe every Sunday evening—take just 10 minutes for a mindful spending check-in.

Open your banking app, look at the last week’s transactions, and ask yourself just two simple questions:

- “What was one purchase this week that I truly valued and that brought me joy?”

- “What was one purchase that, in hindsight, didn’t really align with my goals?”

The first question helps you recognize what spending truly aligns with your values—maybe it was the concert ticket that brought you joy, not the five random coffees. The second question isn’t about guilt, but curiosity. Recognizing purchases that didn’t feel worthwhile helps you gently steer your future spending toward things that matter more. Together, this simple practice builds powerful self-awareness, allowing you to improve your habits without restriction.

As you get more comfortable, you can go deeper. Ask yourself: “How did I feel right before this purchase (stressed, bored, happy)?” or “Does this purchase move me closer to the person I want to be?” The goal isn’t to judge your answers but to observe them with curiosity. This practice of mindful spending slowly rewires your brain to connect spending with values, not just transactions, making it a sustainable budgeting tip for life.

Putting It Into Practice: Your First Month

Feeling overwhelmed? Don’t be. We’re going to make this incredibly easy. Here are three simple actions you can take this week to get started on your behavioral budget.

- Action 1: Calculate Your “Automate” Number. Take 20 minutes and add it up. What’s the total of your crucial savings goals (start small, maybe 10% of your income) and your fixed monthly bills? This is your magic automation number.

- Action 2: Set Up ONE Automatic Transfer. Log in to your online banking portal right now. Seriously, right now. Set up just ONE recurring transfer from your checking account to your savings account for the day after you get paid. You can add more later. The goal today is to start.

- Action 3: Schedule Your Check-in. Open your digital calendar and schedule a 15-minute appointment with yourself for next Sunday called “Mindful Money Check-in.” Setting the time makes it real.

From Financial Stress to Financial Intention

For too long, we’ve been told that financial discipline means more rules, more tracking, and more willpower. The behavioral budget flips that idea on its head. A better budget isn’t about more restriction; it’s about a better system that works with your brain’s natural tendencies, not against them.

The goal here is to reduce financial anxiety and free up your precious mental energy. By automating the important stuff and practicing gentle mindful spending, you stop obsessing over every dollar. You can finally focus on what really matters: living a life that you genuinely value. It’s time to move from a state of constant financial stress to one of calm, clear financial intention.

What has been your biggest frustration with traditional budgeting? Share your experience in the comments below!

{kind=link}