Introduction: The Two Sides of the Same Coin

Let’s paint a picture. It’s 10 PM. You’re scrolling on your phone, and a wave of dread washes over you. You were just checking your bank account, and the numbers aren’t making you happy. That little voice of financial anxiety starts whispering (or, let’s be real, shouting) in your ear. So, what do you do? You close your banking app and immediately open a meditation app, desperately trying to “calm your mind” with a 10-minute guided breathing exercise. You’re trying to fix the symptom—the anxiety—without ever addressing the root cause.

Sound familiar? Not even kidding, this is the digital hamster wheel so many of us are stuck on. We treat our money and our minds like they live in separate houses on opposite sides of town. We use one set of tools to manage our budget and a completely different set to manage the stress our budget (or lack thereof) causes. It’s a disconnected, exhausting cycle. But what if we told you that your money and your mind aren’t just neighbors? They’re roommates. In fact, they share the same brain.

Welcome to the real definition of financial wellness. It’s a concept that goes far beyond spreadsheets and savings rates. True financial wellness isn’t about being a math genius or living a life of extreme frugality. It’s about building a healthy, conscious, and peaceful relationship with your money. It’s about understanding the deep, undeniable link between your financial health and your mental health, and tackling both at the same time. Overlooking this connection is one of the biggest mental traps that lead to stress.

This guide is your starting point. We’re here to ditch the shame, toss out the confusing jargon, and introduce an integrated framework that addresses both your bank account and your well-being. Let’s get started.

Why We’re So Anxious About Money: A Modern Crisis

If you feel stressed about money, please hear us when we say this: You are not alone. Seriously though, you’re not broken, bad with money, or failing. You’re a human being living in a world where financial anxiety has become a silent epidemic. It’s a constant, low-level hum of worry for millions, a feeling that something is wrong, even when you can’t quite put your finger on it.

This isn’t just a feeling; it’s a documented reality. The data we’ve seen is staggering and validates what we all feel in our gut. It’s time to stop blaming ourselves and start understanding the larger forces at play.

The Data Doesn’t Lie

Evidence from numerous studies paints a clear picture. For instance, the Northwestern Mutual 2025 Planning & Progress Study has consistently highlighted financial uncertainty as a major source of stress for Americans. While specific numbers change year to year, the trend is undeniable: an overwhelming majority of people, often figures approaching 9 out of 10, report feeling some level of anxiety about their financial situation.

This isn’t a personal failing; it’s a societal issue. We’re navigating a perfect storm of economic pressures. The cost of everything from housing to groceries seems to be climbing, wages struggle to keep pace, and the weight of student loans feels heavier than ever. Add to that the constant pressure cooker of social media, where everyone seems to be living their best, most luxurious life. It’s a highlight reel of consumption that can make our own reality feel painfully inadequate. This constant comparison fuels a cycle of money and mental health struggles, leading to sleepless nights, strained relationships, and a persistent feeling of being behind. Recognizing this collective experience is the first step toward finding a solution that works.

The Failure of Traditional Tools

So, in response to this pressure, we turn to the tools we’re told will help. We download a shiny new budgeting app, determined to get our spending under control. For a week, we’re diligent. We track every coffee, every subscription, every impulse buy. And then what happens?

The app flashes a notification: “You’ve gone over your ‘Dining Out’ budget by $75!” Instead of feeling empowered, we feel shame. Failure. The app did its job—it tracked the numbers—but it completely ignored the human element. It didn’t know that we were stressed from work and ordered takeout for convenience, or that we were celebrating a friend’s good news.

This is why traditional financial tools so often fail.

- They are Reactive, Not Proactive: They are fantastic at telling you where your money went yesterday. They are terrible at helping you understand the emotional and psychological forces that will dictate where your money goes tomorrow. It’s like a smoke detector that only goes off after the house has burned down.

- They are Tedious and Time-Consuming: Let’s be honest. Manually categorizing every single transaction is a chore. Life gets busy, we miss a few days, and suddenly the data is incomplete and useless. We fall off the wagon, feel guilty, and abandon the whole project.

- They Ignore the “Why”: This is the biggest piece of the puzzle, and it’s where the fascinating field of behavioral finance comes in. Behavioral finance teaches us that our financial decisions are rarely 100% logical. They are driven by emotions, deep-seated habits, cognitive biases, and psychological triggers. A spreadsheet can’t fix a boredom-induced online shopping spree. A pie chart can’t address the anxiety that leads to “retail therapy.” These tools treat the math problem but ignore the mind problem, which is why we need a new blueprint.

The Blueprint for Financial Wellness: 4 Core Principles

Alright, enough about the problem. Let’s get to the solution. Building true financial wellness requires a new approach—one that’s integrated, empathetic, and, most importantly, effective. It’s not about restriction; it’s about intention. It’s not about willpower; it’s about systems. We’ve broken it down into four core principles that form the foundation of this new way of thinking.

1. Reframe Budgeting as “Mindful Spending”

First things first: we need to ditch the word “budget.” For most of us, that word carries the emotional weight of a diet—it implies restriction, scarcity, and saying “no” to things we enjoy. It’s no wonder we avoid it.

Let’s reframe it. Instead of a “budget,” let’s call it a “Mindful Spending Plan.” The goal isn’t to cut back on everything; the goal is to consciously direct your money toward the things that genuinely align with your values and bring you lasting joy and fulfillment. This is the essence of mindful money. It’s about spending with awareness and purpose.

How do we do this?

- Identify Your Core Values: Before you even look at your bank account, take a moment for self-reflection. What truly matters to you? Is it security? Experiences with loved ones? Learning and growth? Creativity? Write down your top 3-5 values.

- Track Without Judgment: For one month, use a simple notebook or a tracking app to see where your money is going. And here’s the key: NO JUDGEMENT. You are not “good” or “bad.” You are a detective gathering data. That’s it.

- Analyze the Gap: At the end of the month, pull out your list of values. Look at your spending. Ask yourself: “How much of my spending actually supported my core values?” You might be surprised. You might find you spent $200 on mindless delivery orders (value: convenience) but only $20 on a book or class (value: learning).

- Create Your Plan: Now, you can create your Mindful Spending Plan. It’s not about cutting out the lattes if they bring you genuine daily joy. It’s about consciously deciding if you’d rather have those lattes or redirect that money toward something that aligns more with your values, like saving for your next great adventure. For others, it could mean setting a long-term savings goal for a truly transformative experience, like a rejuvenating Ayurvedic Panchkarma treatment and yoga retreat, as an ultimate investment in their mental and physical peace. This process transforms your finances from a source of shame into a tool for building a life you love.

2. Build Systems to Reduce Willpower

Willpower is a finite resource. Think of it like a muscle. You can use it for a while, but eventually, it gets tired. Trying to rely on sheer willpower to make good financial decisions every single day is a recipe for exhaustion and failure. We experience “decision fatigue,” and when we’re tired, we tend to make the easy choice, not the right one.

The secret? Make the right choice the easy choice. The way we do that is through automation. Building systems that work for you in the background is the core of smarter living. It removes the daily temptation and internal debate, making progress effortless and helping you make powerful financial decisions when it counts.

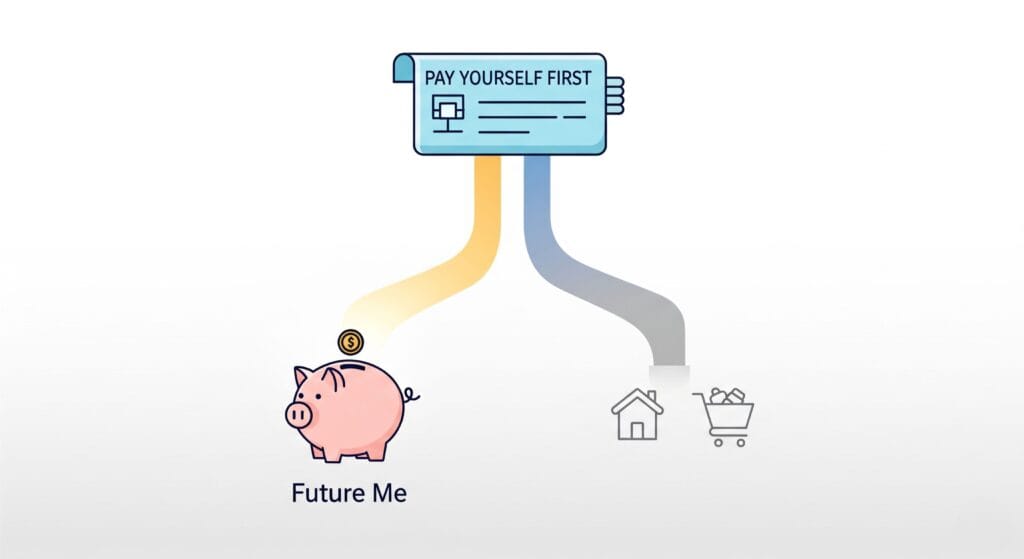

- Pay Yourself First, Automatically: This is the golden rule. Set up an automatic, recurring transfer from your checking account to your high-yield savings account for the day after you get paid. Even if it’s just $25 to start. The money is gone before you even have a chance to miss it or debate spending it.

- Automate Your Debt Payments: If you have loans or credit card debt, set up automatic minimum payments. This ensures you never get hit with a late fee (which is literally throwing money away) and reduces the mental load of remembering due dates.

- Automate Your Bills: For predictable bills like your phone, internet, or streaming services, set up autopay. This frees up mental energy and ensures your services are never interrupted because of a simple oversight.

By automating the important things, you conserve your precious willpower for the decisions that really matter. You’re no longer fighting a daily battle; you’ve built a fortress that defends your financial goals for you.

3. Connect Your Moods to Your Money

This principle is where financial wellness truly bridges the gap between money and mental health. Our spending is deeply emotional. We spend when we’re sad to feel better. We spend when we’re bored for a little thrill. We spend when we’re celebrating because we feel like we “deserve it.” Ignoring this connection is like trying to fix a leaky pipe by only mopping the floor.

The key is to cultivate awareness. We need to become conscious observers of our own behavior. A powerful tool for this is a “Money Journal.” It doesn’t have to be complicated. For a week, every time you make a non-essential purchase, jot down a few things:

- What did I buy?

- How much did it cost?

- How was I feeling right before I bought it? (Stressed, bored, happy, tired?)

- What was I hoping this purchase would accomplish for me?

This isn’t about shaming yourself; it’s about identifying patterns. You might notice you always shop online after a stressful day at work. Or that you tend to overspend on food when you feel lonely. This is behavioral finance in action.

Once you see the pattern, you can create a plan to interrupt it. If stress is your trigger, what’s a free or low-cost alternative to shopping? A walk outside? Calling a friend? A 5-minute meditation? Finding healthier coping mechanisms, like staying active at home, can be a game-changer. By finding healthier ways to manage the underlying emotion, you remove the financial symptom. It’s about asking “why” before you buy.

For those who want to try a powerful, guided exercise to directly address feelings of financial fear, the tapping technique (EFT) can be incredibly effective. Below is a video from expert Brad Yates that will walk you through the process.

For many, simply building this awareness is enough to create change. However, if you find that these emotional spending triggers are persistent or tied to deeper feelings of anxiety or stress, it can be incredibly empowering to speak with someone. Professional support can provide you with tools to manage these emotions effectively, breaking the cycle for good. Services like online therapy are making it more accessible and affordable than ever to get that support right from your home.

This post contains affiliate links. That means if you click a product link and make a purchase, we may earn a small commission—at no extra cost to you. As an Amazon Associate, we earn from qualifying purchases. It’s one of the ways we keep this website running and continue bringing you helpful content. So, thank you—seriously, your support means the world to us!

4. Prioritize Financial Literacy as Self-Care

For many, the idea of “financial literacy” sounds about as appealing as a root canal. It seems complicated, boring, and overwhelming. We’re here to rebrand it. Learning about money is not a chore; it is one of the most fundamental acts of self-care you can practice.

Think about it. We learn about nutrition to care for our bodies. We go to therapy or practice mindfulness to care for our minds. Why wouldn’t we learn about the system that so profoundly impacts our stress levels, our opportunities, and our future?

Prioritizing financial literacy is an act of empowerment. It’s about taking control and building confidence. And you don’t need to become a Wall Street guru. The goal is simply to understand the basics so you can make informed decisions for yourself. Here are some gentle entry points:

- Read One Article a Week: Commit to reading one article from a trusted source, like our Guide page, each week.

- Listen to a Podcast: There are tons of fun, engaging podcasts that break down financial topics in an accessible way. Find one that matches your vibe.

- Read One of the best personal finance books: Choose a classic or a modern guide and read a chapter a week. You can also explore other top empowering books that inspire growth to build a broader sense of self-assurance.

Knowledge replaces fear with confidence. The more you understand, the less anxious you’ll feel. You’ll start to see your finances not as a source of dread, but as a tool you can wield to build a more secure and peaceful life. This is the ultimate goal of financial wellness. If you’d like to know more about us and our philosophy, you can check out our About page.

Your First Steps to Financial Calm: A Practical Guide

Theory is great, but action is what creates change. The four principles are the “what,” but this section is the “how”—right now. Let’s make financial wellness tangible with three simple, actionable steps you can take today to immediately reduce financial anxiety and start building momentum.

The “Pre-Purchase Pause”

Impulse spending is one of the biggest budget-busters and anxiety-inducers. It’s that moment you see something online or in a store and your brain screams, “I need that!” before your logic can catch up. We can short-circuit this impulse with a simple mindfulness exercise we call the “Pre-Purchase Pause.” It takes two minutes.

Here’s the script:

- Stop and Hold: Whether it’s in your physical hands or your online shopping cart, just stop. Don’t click “Buy Now.”

- Take Three Deep Breaths: Inhale slowly through your nose, and exhale slowly through your mouth. Do this three times. This simple act engages your parasympathetic nervous system, calming the “fight or flight” impulse and giving your rational brain a chance to come online.

- Ask Three Questions: Ask yourself these questions honestly.

- Why? “Why do I really want this?” Is it a genuine need, or am I trying to soothe an emotion like boredom, stress, or sadness?

- Can I? “Can I truly afford this right now without creating future stress for myself?” This isn’t just about whether the money is in your account, but the emotional cost of that money leaving it.

- Where? “Where will this item be in six months?” Will it be a cherished part of your life, or will it be forgotten in a closet, a drawer, or worse, a landfill?

That’s it. Sometimes you’ll still decide to buy the thing, but now it will be a conscious choice, not a reaction. More often than not, this pause will be all you need to realize you don’t actually need it, saving you money and future regret.

Automate One Thing, Today

We talked about the power of systems. Let’s build your first one right now. It will take less than five minutes and is one of the most powerful first steps toward building wealth and peace of mind. We’re going to automate your savings.

- Log In: Open your primary bank’s mobile app or website.

- Find “Transfers”: Navigate to the section for making transfers between your accounts. Look for an option called “Automatic Transfers,” “Recurring Transfers,” or “Scheduled Transfers.”

- Set It Up:

- From: Your Checking Account.

- To: Your Savings Account. (If you don’t have a separate one, open one! It’s crucial for your mindful money practice).

- Amount: Start small. Seriously. Even $10 or $20. The amount doesn’t matter as much as building the habit. You can always increase it later.

- Frequency: Set it for “Weekly” or “Bi-Weekly,” and schedule it for the day after your paycheck usually hits.

- Confirm and Celebrate: Hit that confirm button and do a little happy dance. You just paid your future self. You put your savings on autopilot and took a massive step toward long-term financial wellness.

Conduct a “Financial Check-in”

One of the biggest drivers of financial anxiety is avoidance. We’re afraid to look at our accounts because we’re afraid of what we’ll find. A regular, non-judgemental “Financial Check-in” can transform this fear into a feeling of control. It’s not about judging your past; it’s about informing your future.

Once a week or once a month, set aside 15 minutes. Put on some music, grab a cup of tea, and ask yourself three simple questions. Write down the answers.

- What is one thing that went well with my money recently? Did you remember to use a coupon? Did you say no to an impulse buy? Did you pay a bill on time? Find a win, no matter how small, and celebrate it. This builds a positive association with your finances.

- What is one area that felt stressful? Was it grocery costs? A surprise car repair? The looming feeling of a credit card bill? Name it. Acknowledging the stress point is the first step to creating a plan to address it. There is no judgment here, only awareness.

- What is one small, gentle change I can make next month to address that stress? This isn’t about a massive overhaul. If groceries were stressful, maybe the small change is planning two meals ahead of time. If it was a surprise bill, maybe the change is starting that automatic transfer of $20 to an “emergency fund.” The goal is small, sustainable progress. This regular check-in transforms financial fear into a feeling of control, which is crucial whether you’re saving for retirement or planning for a budget-friendly dream wedding.

Conclusion: Wellness is the New Wealth

For too long, we’ve chased wealth as the ultimate goal. We’ve been told that a bigger number in our bank account is the key to happiness. But as we’ve explored, that’s only half the story. A person can have millions and still be consumed by financial anxiety, while someone with a modest income can feel a profound sense of peace and security.

The goal is not just wealth. The goal is wellness. True financial wellness is the ultimate prize. It’s the quiet confidence that comes from knowing you have a plan. It’s the freedom from the constant, nagging worry about money. It’s the ability to use your financial resources, whatever they may be, to build a life that is rich in joy, purpose, and peace of mind.

Managing your money and managing your mind are not two separate tasks. They are one and the same. By embracing mindful money practices, building smart systems, understanding our emotional triggers, and committing to learning, we can heal our relationship with our finances. We can move from a state of anxiety to a state of empowerment. This is the new definition of wealth. It’s a calm mind, a clear plan, and a life lived with intention.

If you have any questions or want to start a conversation, feel free to Contact Us. We’re here to support you on this journey.

What’s the biggest source of your financial anxiety? Share your thoughts in the comments below. Let’s tackle this together.

{kind=link}